Quiet Index, Loud Internals

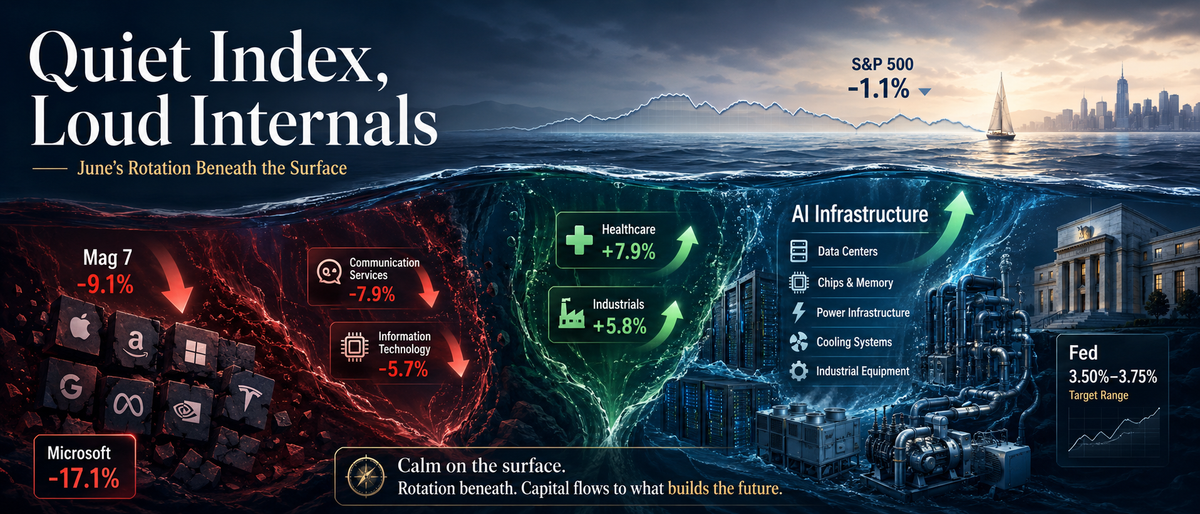

The S&P 500 finished June down only 1.1%, but the calm index hid a much louder market underneath. The Mag Seven lagged, Microsoft fell 17.1%, healthcare and industrials rallied, and AI leadership moved toward the physical infrastructure layer.

June looked calmer than it was.

The S&P 500 finished the month down 1.1%. That is not the kind of index move that usually defines a market regime. It does not look like a panic. It does not look like broad liquidation. It looks manageable.

But underneath the index, June was anything but quiet.

The important story was rotation.

The Magnificent Seven became the Lag Seven. The Roundhill Magnificent Seven ETF finished June down 9.1%, after closing June 25 down 13.6% month-to-date. Microsoft fell 17.1% in June. For a company that still had a market value of roughly $2.8 trillion at month-end, that was not normal noise. It was the market taking a much harder look at the cost of AI leadership.

That is the central point.

The market did not reject AI. It rejected unquestioned AI spending.

For much of the AI cycle, investors rewarded exposure. If a company had AI scale, AI distribution, AI data, AI cloud capacity, or AI ambition, the market often gave it the benefit of the doubt. In June, the question changed. It was no longer enough to say a company was exposed to AI. The harder question became whether the company could earn attractive returns on the capital being deployed.

That matters because the largest AI platforms are becoming more capital intensive.

Data centers are expensive. Power is expensive. Memory, chips, networking, cooling, and model infrastructure are expensive. The hyperscalers may still be extraordinary businesses, but extraordinary businesses can still face valuation pressure when the market starts asking whether the next dollar of AI capex earns enough return.

Microsoft became the cleanest example. The company is still one of the strongest software and cloud franchises in the world. But in June, investors were not rewarding strength by default. They were asking about capital intensity, margins, AI monetization, and duration. When rates are no longer clearly falling, those questions become more important.

At the same time, capital did not leave the AI theme.

It moved within it.

The market started separating AI spenders from AI infrastructure beneficiaries. That is why the physical layer of AI became so important. Micron had a market cap around $1.32 trillion by the start of July. AMD was around $959 billion, close to the trillion-dollar line. Intel was around $710 billion, not yet in that club, but large enough again to matter in the AI infrastructure conversation.

That is a major change in market psychology.

The old assumption was that the mega-cap platforms would capture most of the value because they owned the customer, the cloud, the data, and the distribution. June showed a more complicated picture. The companies writing the checks for AI capacity were being questioned. The companies supplying the memory, compute, manufacturing capacity, and infrastructure required to build that capacity were being rewarded.

This is why the index alone was misleading.

At the sector level, the split was dramatic. Communication Services fell 7.9%. Information Technology fell 5.7%. Healthcare rose 7.9%. Industrials rose 5.8%.

That is not a quiet market.

That is a market repricing leadership.

The index looked manageable because the winners and losers offset each other. Former leaders dragged. Healthcare worked. Industrials worked. Defensives had a bid. AI infrastructure names absorbed capital. The average portfolio experience depended much more on what was owned underneath the benchmark than on the benchmark return itself.

This is one of the reasons we pay close attention to internals.

An index is an aggregation. It can look calm while its components are moving violently in different directions. It can hide concentration risk when leadership is narrow. It can also hide opportunity when leadership broadens. The headline return is useful, but it is not the full market.

June was a reminder that market risk is not only about direction.

It is also about composition.

The macro backdrop made that rotation more forceful. The Federal Reserve held the policy rate at 3.50% to 3.75% on June 17. The hold was not the important part. The important part was the message: economic activity was still expanding at a solid pace, while inflation remained elevated relative to the Fed's 2% goal.

That is not the backdrop long-duration growth investors wanted.

When the market expects rate cuts, it can forgive a lot of future cash-flow assumptions. When the market starts to price in the possibility that rates stay higher, or even move higher, it becomes much less forgiving. Expensive growth, crowded ownership, and heavy capex all become more vulnerable.

Gold confirmed the same message from another angle.

Bullion was down more than 11% in June and was on track for its worst quarterly performance since 2013. That matters because June was not a classic fear month. Investors were not simply hiding in gold while selling equities. They were repricing rates, positioning, and leadership concentration.

In other words, this was not a simple risk-off month.

It was a deconcentration month.

Capital moved away from crowded ownership and toward areas where the market saw more immediate earnings support, better capital efficiency, or less dependence on distant assumptions. That does not mean the old leaders are broken. It means the market became less willing to pay the same multiple for the same narrative without clearer evidence of return on capital.

For Runtime, this is the durable lesson.

Static mega-cap ownership is not the same as adaptive exposure. A portfolio can look diversified because it owns an index, while still being highly exposed to one leadership cluster, one valuation regime, and one narrative. When that narrative changes, the internal rotation can matter more than the headline index move.

Our objective is not to predict every rotation in advance. That is not the standard we believe investors should require from a process. The more practical objective is to build systems that can operate through changing leadership, changing volatility, changing rates, and changing market participation.

Markets do not always announce regime shifts through crashes.

Sometimes they announce them through internals.

June was one of those months. The index was quiet. The market underneath was loud. The Mag Seven became the Lag Seven, AI leadership moved toward the infrastructure layer, healthcare and industrials gained ground, the Fed became a headwind again, and gold confirmed that this was not simply a flight-to-safety episode.

The clean takeaway is this:

June rewarded adaptive exposure, not static mega-cap ownership.

Engineered compounding,

Deniz Erkan

This communication is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security. Any offer or solicitation will be made only pursuant to definitive offering documents and in accordance with applicable law.